Where did all the money go?

The first programme was worth 73 billion euros, 52.9 billion of which came in the form of bilateral loans from eurozone members states. Another 20.1 billion euros was provided by the IMF.

The loans from the second programme agreed in March 2012 currently stand at 153.7 billion euros. The eurozone’s part is broadly completed as the EFSF has disbursed 141.8 billion with one last tranche of 1.8 billion remaining. The IMF has provided 11.8 billion of financing to date, with its involvement due to run to February 2016.

The combined eurozone involvement in Greece comes to 194.8 billion euros (107 percent of GDP), while the IMF total stands at 31.9 billions (18 percent of GDP).

These are staggering figures: No other nation has received this volume of loans in a period of 4.5 years.

From European Commission review documents, IMF evaluation reports, Finance Ministry budget documents and Hellenic Statistical Authority (ELSTAT) publications we pieced together roughly which financing holes this approximately quarter of a trillion euros closed.

Greece covered some of its financing needs during the period in question via a number of its own sources. The issuance of a 3- and a 5-year bonds in 2014 of 3 and 1.5 billion euros respectively, the increase of the stock of T-bills by 10 billion euros, the use of cash reserves of government bodies via repos worth 7 billion and privatization proceeds in the range of 2.4 billion, provided a total of 24 billion euros of own financing.

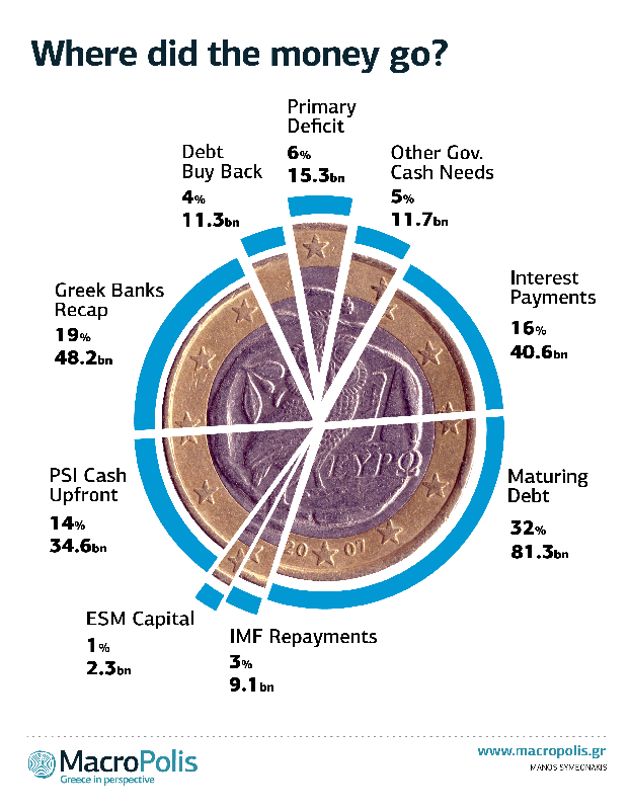

There seems to be a general misconception that feeds a misleading narrative in which the loans were used to keep the Greek state afloat, maintain its basic operations and pay salaries of doctors, teachers and policemen. Only last week Spanish Finance Minister Luis de Guindos made claims along these lines.

"Greece received 210 billion euros from the eurozone, including 26 billion euros for example from Spain," he said. “Thanks to this financing, which Greece could not get from financial markets, it was able to maintain all of its public services... to pay its doctors, its police, its retirees, thanks to this solidarity."

This is only part of the story, though. Indeed, Greece started the fiscal consolidation effort with a deficit before interest payments of circa 24 billion euros in 2009 and was running a primary deficit in 2010, 2011 and 2012. From 2013 onwards, though, revenues exceeded expenses and no financing was needed to cover state operations.

The brutal belt tightening meant that only just over 15 billion euros of troika loans were used for state operations. Combined with some other government financing needs (mostly relating to repayments of arrears that accumulated in the first two years of the crisis) the combined allocation to the Greek state’s operating needs was just 11 percent of the total funding, at circa 27 billion euros.

The financing breakdown speaks to the eurozone's objection to any form of debt restructuring at the very start of the Greek crisis. Roughly half of the financing was provided for debt servicing. From the loans, 81 billion was used to meet maturing debt obligations and for interest payments that exceeded 40 billion euros, almost 122 billion euros in total.

The second largest chunk of troika loans relates to debt reduction exercises. When lenders considered Greece sufficiently ring-fenced and core eurozone banks had reduced their Greek exposure, they decided to place the burden of the problem on private bondholders in February 2012 with the Private Sector Initiative (PSI). This was followed by the debt buyback in the end of 2012.

During the PSI, bondholders were offered new bonds with a face value equal to 31.5 percent of the face amount of those exchanged. They were also given sweeteners in the form of cash-equivalent EFSF notes maturing within 24 months for 15 percent of the face value of the debt exchanged. Also, they were offered short terms EFSF notes for the accrued interest. This totalled 34.6 billion euros or 14 percent of the combined financing needs.

An added 11.3 billion euros was used to buy back over 30 billion euros worth of debt in the second debt reduction initiative of 2012.

To support its banks from the losses incurred in the PSI and the rapidly deteriorating loan portfolios as a result of the deep crisis which saw non-performing loans soaring from 8 percent to 34 percent, Greece borrowed another 48.2 billion euros for bank recapitalisations, resolutions and the restructuring of the banking sector. An amount of 11.6 billion remains unused and could form the precautionary line of the eurozone after the end of the European side of the current programme.

The combined amount of the three initiatives reached 94 billion euros, more than a third of the total financing needs.

Greece started repaying last year the IMF loans supplied during the Stand By Arrangement of the first programme. A total of 9.1 billion euros was paid back by the end of 2014.

Greece also had to participate in the paid in capital of the European Stability Mechanism, to the tune of 2.3 billion euros.

- See more at: http://www.macropolis.gr/