According to a recent poll, more than 65% of Germans think they would be better off without the euro. In the face of this, any talk about Greece staying or leaving the euro is, in my opinion, a red herring. The real issue now is whether Germany will exit the euro (FXE) before Greece does.

Germany, with substantial industrial know-how after the end of WWII, and although it lost the war, managed to grow an economy based on innovation and high quality. Some may not know, for example, that a digital computer was built in Germany by Konrad Zuse in 1938, it was called the Z1, and its improved versions, the Z2 and Z3, were used to design fighter planes1. Although most people associate the birth of the digital computer with work done in the USA and England, and associate Germany with innovation in heavy machinery, historical facts may be challenging such views.

The German industrial capacity and established brand names like Mercedes-Benz, BMW, Siemens (SI), and MAN, to name a few, faced a serious economic challenge in the 1960s: Other European countries would constantly devalue their currency in order to become competitive exporters mainly of agricultural, textile and some durable goods, and as a result Germany's high quality products were becoming more expensive and hard to sell. The euro solution aimed at facilitating a positive expectation game for Germany (and also partly for France) in trading goods with developing countries like Spain, Portugal, Greece, Italy and others, through the abolition of sovereign currencies. In exchange, the nations that abolished their sovereign currency right would supposedly benefit from a common strong currency and low interest rates, as well as, from the possibility of becoming a part in the future of a United States of Europe to compete with the all mighty United States of America and Asian countries.

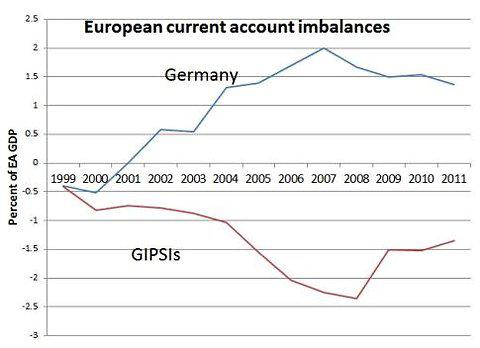

Several European nations bought into this scheme, each for their own reasons. However, the transfer of wealth from those nations to Germany started immediately and continued without this final unification ever taking place. At the same time, nations that should have interest rates in the 10% - 15% range based on sovereign currency enjoyed very low levels of interest rates for an extended period of time. This further facilitated the wealth transfer from most of the weak countries to Germany because consumers in those developing countries could borrow at low interest rates to buy the German products free of any import taxes that would normally be imposed if the European Union did not exist. Paul Krugman has called this process "a capital flow bubble from north to south induced by the euro" in an article in his blog, where he included the upper chart that illustrates the growth of EU current account imbalances over the years.

The rise of China further contributed to the growing deficits of most European countries, especially in the south, where traditional industries, like textiles and small durable goods manufacturing, disappeared with the advent of cheap Chinese imports. The positive expectation game for Germany achieved via the use of a common currency reached its peak when the debt of the countries in the south of Europe reached levels that could not be financed by the markets any longer. The problems emerged either as a high government deficit or as a banking liquidity problem. In countries where the banks directly financed the standard of living of consumers, like in Ireland and in Spain for example, a banking problem emerged. In countries like Greece, where the government issued bonds to be able to act as an employer of last resort, the problem was of a high deficit and government debt.

There is no positive expectation for Germany in the EU at this point because the failed nations want everyone to share the losses. As a matter of fact, it appears that in order for the EU to survive, the Germans should start giving back their profits to rebalance the system. That could take the form of money printing, or of issuing eurobonds, or even of provision of German guaranties to other nations for financing their debt. As a result, if EU and the euro must continue to exist, the German standard of living must decline. This appears to be unacceptable to Germans as the recent poll showed.

One alternative is for Germany to get out of the euro. The cost will be high in the short term because the newly adopted German currency will appreciate substantially in relation to the euro and exports will slow down. However, Germany will be able to keep its current surplus and invest in other European countries by buying cheap assets, something that cannot be done with the euro at this point because recent experience has shown that internal devaluation has a minimum impact on asset prices and such process mainly affects the salaries of workers. Essentially, if Germany exits the euro, that will prevent its wealth from getting diluted, and it can use it to assist other countries in rebuilding. If Germany finances those countries now, it is possible that no positive effect will result in the longer-term because of the structural problems in their economies.

A German Exit Before A Greek Collapse

The chances are higher that Germany will get out of the euro before Greece does for all the reasons just detailed. Greece does not want to do that because it would result in local hyperinflation in the short-term and financial chaos. There is a another, very low probability scenario, that EU countries will set aside their financial differences and only focus on European integration. I think this is an idealistic situation and given recent European history and the tremendous cultural gaps that exist between the various countries the probability is extremely low but if it ever happens it would be like a miracle of the 21st century.

To summarize, I will not be surprised if voices from Germany for an exit from the euro become louder in the next few months. The impact of such a scenario on the markets will be noticeable with increased volatility and wild swings, especially in the foreign exchange markets. All investors and traders should keep in mind this scenario and be prepared. Further signs of increasing public support in Germany for a euro exit could send the dollar higher and FXE, the ETF that tracks EUR/USD movements, lower. This scenario could also affect stock prices with a correction in S&P 500 and SPY (SPY) of more than 10%. Eventually, the volatility will decrease and stock markets will rebound. After all, Germany and the EU will still be in place and the only change will be the addition of another strong currency in worldwide reserves.

1. The company that Zuse started, ZUSE AG, which developed digital computers for industrial automation use, was bought by Siemens.